Free Trade with MERCOSUR: An attractive opportunity for the UK?

Written by: Manuel Tong Koecklin

After a negotiation process characterised by long periods of stagnations and disagreements[1], on the 17th of January, a Partnership Agreement was signed between the European Union and the four founding members of the Southern Common Market (MERCOSUR, as known in Spanish): Argentina, Brazil, Paraguay and Uruguay[2]. This free trade agreement is meant to eliminate tariffs on 91% of EU exports to the South American bloc. This will be done over a 15-year phase-in period, paired with the removal of duties on 92% of MERCOSUR goods sold to the EU, within a 10-year timeframe.

There is uncertainty regarding the ratification and implementation of this deal, due to a recent decision by the European Parliament to refer the agreement to the EU Court of Justice. Nevertheless, the economic size of the parties involved (estimated at 18% of the world’s GDP), along with the current context in which traditional large trading partners are becoming less reliable, has generated global interest. Such deal could constitute an example for other economies seeking to secure free trade with like-minded partners. It would allow them to diversify their trade portfolio and diminish their dependence on potentially problematic counterparts.

If the deal goes ahead, EU exporters will secure preferential access to the MERCOSUR market, avoiding high tariffs for goods like cars (35%), machinery (up to 20%), spirits (up to 35%) and pharmaceuticals (up to 14%).

Meanwhile, the UK (which would have been part of this agreement in a non-Brexit scenario), will continue to trade under existing MFN terms. Last September, the UK Trade Minister stated that securing a deal with MERCOSUR would be a “no-brainer”[3]. However, formal negotiations have not begun yet. This leaves the UK behind compared to European parties like the EU and EFTA, which have both signed agreements with MERCOSUR.

To what extent would securing free access to the MERCOSUR market be an opportunity for the UK? Which sectors/goods in the UK would benefit the most from this potential partnership? And to what extent might UK firms be losing out compared to their EU counterparts?

Based on trade data [4], it looks like the UK is not missing out on much. On average, the four MERCOSUR partners only account for 0.68% of UK goods exports and 0.70% of imports between 2018 and 2024. Comparable figures are slightly larger for the EU27: – 0.79% for exports and 0.84% for imports.

Most UK and EU trade with MERCOSUR is with Brazil, averaging over 73% of trade with the bloc in 2018-2024. The EU represents an average of 14.33% of MERCOSUR exports and 17.93% of imports, whereas the UK accounts for around 1% of MERCOSUR trade.

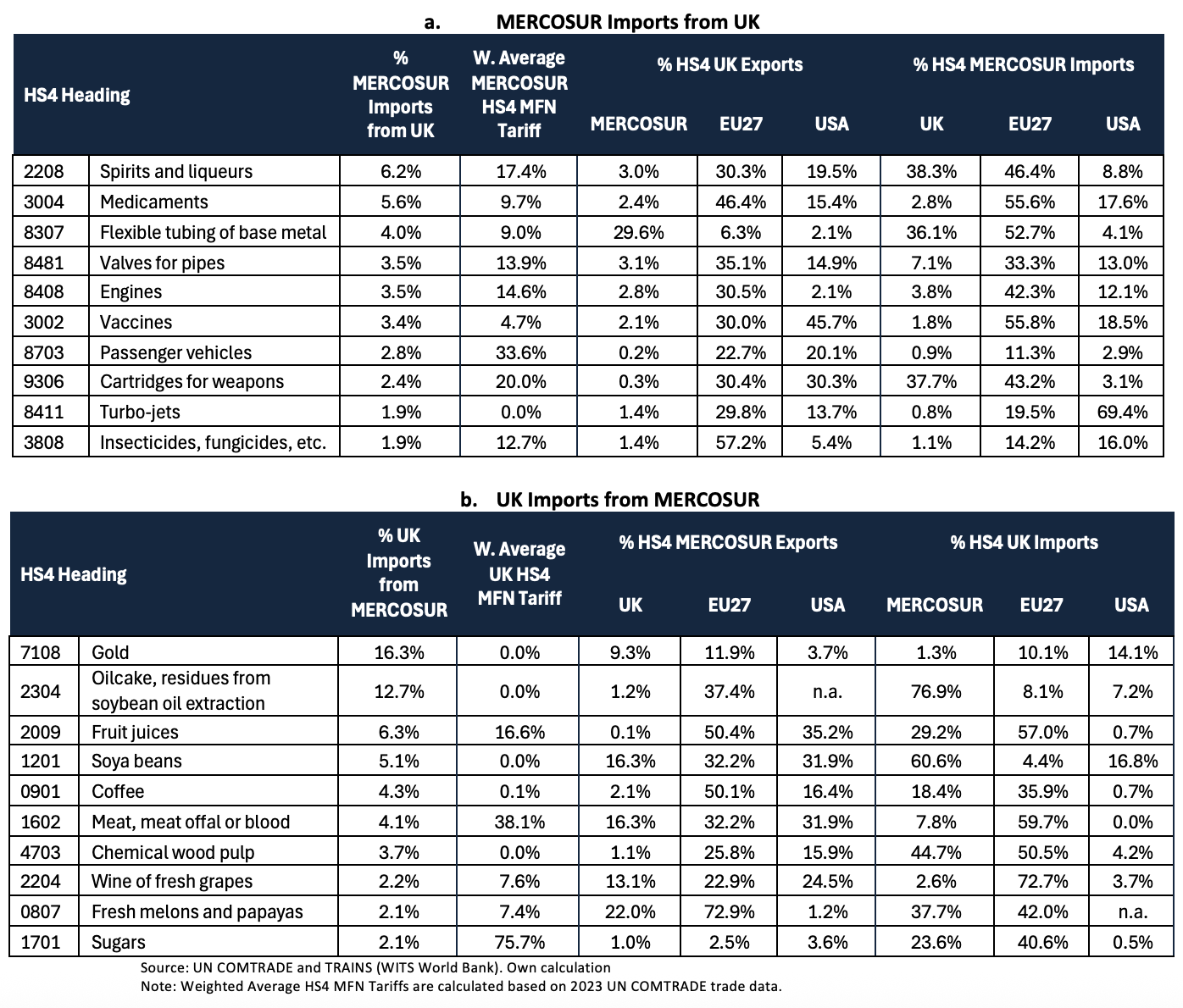

Aggregate figures, however, conceal how different sectors or products might be affected. Table 1 is based on data which covers over 1200 product categories[5], and shows the top 10 goods purchased by MERCOSUR from the UK, and the top 10 UK imports from MERCOSUR, based on total bilateral flows in 2024.

There is a considerable overlap between the UK top 10, and those of the EU27, with medicaments, vehicles and their parts accounting for the largest shares of goods sold to MERCOSUR, and agrifood products derived from the soybean, coffee and fruits industries dominating imports.

Table 1 –Top 10 HS4 Headings Traded between the UK and MERCOSUR – 2024

Focusing on MERCOSUR imports from the UK, Table 1.a, column 1, shows the share of each product in UK exports to Mercosur; column 2 gives the average Most Favoured Nation (MFN) tariff applied by MERCOSUR. The subsequent three columns show, for each product, the share of UK exports going to MERCOSUR, the EU and the US. Finally, the last three columns show how important the UK, the EU and the US are for MERCOSUR as a source of these goods.

Consider spirits and liqueurs (HS4 2208), the UK’s top export to MERCOSUR. Figures show that MERCOSUR heavily depends on the UK (38.3%) and the EU27 countries (46.4%) for its imports. However, MERCOSUR does not represent a big market for the UK, accounting for only 3% of exports.

This is presumably due in part to the high average tariff (17.4%), and in part to the size of the MERCOSUR market. The high tariff suggests that a UK-MERCOSUR deal could provide significant opportunities, even if these may be staggered over time, as under the signed EU-MERCOSUR deal, most 2208 products are liberalised over 4 years.

The same can be argued for ‘flexible tubing of base metal’ (HS4 8307), where tariffs are high (close to 10%), and the UK is already a significant supplier. Indeed, a trade deal would help UK exporters avoid high tariffs for products like passenger vehicles (33.6%), engines (14.6%), valves for pipes (13.9%), insecticides (12.7%), among others. In terms of partner diversification, a deal with MERCOSUR could help the UK reduce dependence on the United States in the sales of vaccines (45.7% going to the US), passenger vehicles, medicaments, turbo-jets or valves for pipes.

Regarding UK imports, Table 1.b shows these are dominated by raw materials like gold and agrifood products (including fruit juices, soybeans, and coffee). MERCOSUR is the largest foreign supplier for many of these products, with shares of up to 76.9% for residues from soybean oil extraction (HS4 2304). However, many of them already receive zero-tariff treatment under the UK MFN scheme.

For the UK, the most perceptible benefits from an FTA with MERCOSUR arise on the export side, given the current large tariffs UK goods are subject to in that market. It may also provide the opportunity for the UK to gradually reorient its trade portfolio. This is perhaps more relevant in a context in which certainty and predictability of trade relations and underlying rules are under strain.

Services trade, public procurement, investment and environment are still to be analysed. Nevertheless, an initial look at the goods trade data shows that MERCOSUR is likely to be an attractive opportunity for certain UK industries. Another aspect for future analysis is the extent to which improved access to the EU market for MERCOSUR may compete with UK exports to the EU. The EU’s experience could serve the UK as a reference on how to manage potential opposition from sensitive stakeholders like farmers, attempt to attain more generous liberalisation schedules from MERCOSUR for certain goods, and even pursue the inclusion of Bolivia, another full MERCOSUR member[6].

Footnotes

[1] https://ecipe.org/insights/eu-mercosur-agreement-is-not-old/

[2] Bolivia is also a full member of MERCOSUR but is not part of this agreement, since it was granted that condition in December 2023, when the negotiations between the four founding members and the EU were already in course.

[3] https://www.politico.eu/article/uk-trade-minister-says-uk-mercosur-trade-deal-a-no-brainer/

[4] UN COMTRADE data, available on the World Bank’s World Integrated Trade Solution (WITS).

[5] At the HS 4-digit level.

[6] Indeed, including Bolivia in a potential UK-MERCOSUR deal would be significant for UK exporters of spirits and liqueurs (HS4 2208) or chemical products (HS4 3811). These are currently subject to Bolivia’s MFN tariffs of 40% and 10%, respectively.

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Republishing guidelines:

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to the original resource on our website. We do not publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.